In the modern Indian financial landscape, a personal loan has become one of the most vital tools for managing liquidity gaps and fulfilling life’s major milestones. Whether you are planning a dream wedding, tackling an unexpected medical emergency, funding higher education, or renovating your home, understanding the criteria for approval is the first step toward financial freedom. If you are exploring instant personal loan apps in India with fast approval, understanding eligibility becomes very important. However, nearly 32% of loan applications in India are rejected simply because borrowers do not fully understand the multi-layered framework lenders use to assess risk.

At MoneyMonk, we believe that transparency is the key to a stress-free borrowing experience. This comprehensive guide provides an authority-based deep dive into every factor that determines your personal loan eligibility in India. You can also apply for an instant personal loan online without paperwork through digital platforms, ensuring you are prepared to secure the funds you need with confidence.

1. What Exactly is a Personal Loan?

Before diving into the eligibility “how-to,” it is essential to understand the “what”.A personal loan is an unsecured credit facility. Today, many borrowers prefer to apply for a personal loan through a trusted digital platform for faster approvals, meaning you do not need to pledge collateral like gold or property to secure the funds. Because the lender takes on higher risk without security, they rely heavily on your “intent to pay” and “capacity to pay”.

The principal amount and interest are repaid through Equated Monthly Installments (EMIs) over a pre-determined tenure, which typically ranges from 12 to 84 months depending on the lender. At MoneyMonk, we specialize in digital personal loans with a focus on speed and convenience, offering amounts ranging from ₹25,000 to ₹3 Lakhs through a 100% online process.

2. The Core Pillars of Personal Loan Eligibility

Lenders in India use a sophisticated assessment funnel to evaluate your application. This involves a combination of demographic markers, professional stability, and quantitative financial ratios.

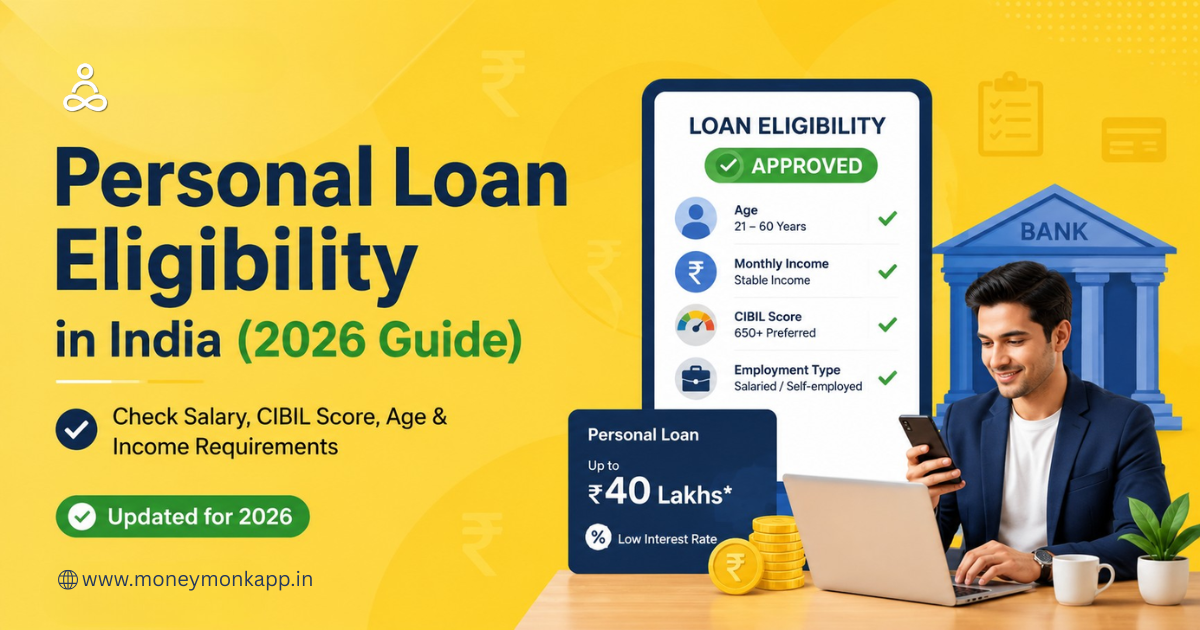

A. Age Criteria: The Earning Window

Age is used as a proxy for the remaining duration of your peak earning years. Most lenders have strict age thresholds. Before applying, it is always smart to check your personal loan eligibility online instantly, to ensure the loan is repaid before retirement.

- Minimum Age: Usually 18 to 21 years at the time of application.

- Maximum Age: Generally capped at 60 to 65 years at the end of the loan tenure for salaried individuals.

- MoneyMonk Requirement: Applicants must be Indian Citizens over 21 years of age.

B. Income Thresholds: Your Capacity to Repay

Income is the primary indicator of your ability to service a loan. You can also check loan eligibility without affecting your credit score before applying. Lenders set minimum monthly income requirements based on your city of residence and employment type.

- Metro vs. Non-Metro: Minimum income requirements are often higher in metro cities like Mumbai or Bangalore (ranging from ₹25,000 to ₹30,000) compared to Tier-2 or rural areas (starting from ₹15,000).

- MoneyMonk Requirement: We require a stable monthly source of income of at least ₹18,000.

- Annual Household Income: For certain digital products, an annual household income greater than ₹3 Lakhs is preferred.

C. Employment Type and Stability

The nature of your income source significantly impacts the perceived risk. Always choose reliable personal loan platforms with transparent processes for better approval chances.

- Salaried Individuals: Employees of government bodies, PSUs, and reputed private MNCs are high-priority segments due to job security. Lenders typically look for a total work experience of at least 1–2 years, with at least 6–12 months in the current organization.

- Self-Employed Professionals: Doctors, CAs, and entrepreneurs face more stringent criteria, often requiring a minimum “Business Vintage” of 3 to 5 years.

- Stability Matters: Frequent job changes (job-hopping) raise red flags, as they suggest professional instability and a higher risk of default.

3. The Ultimate Arbiter: Understanding Your CIBIL Score

In the unsecured credit market, your CIBIL score is the most critical filter lenders use. It is always better to manage your personal loan eligibility using digital tools before applying, to evaluate your reliability. This three-digit number, ranging from 300 to 900, acts as your financial report card.

The Impact of Score Tiers (2026 Benchmarks)

| CIBIL Score Range | Risk Perception | Likely Outcome |

| 750 – 900 | Excellent / Prime | Near-instant approval and the lowest interest rates. |

| 700 – 749 | Good | High approval chances with competitive terms. |

| 650 – 699 | Fair / Average | Approval possible but with higher interest rates and manual scrutiny. |

| Below 650 | Poor / High Risk | Very high rejection rates; may require secured loan alternatives. |

Factors That Build Your Score

- Payment History (35% Weight): Punctual repayment of previous EMIs and credit card bills is the single most important factor.

- Credit Utilization Ratio (CUR): You should ideally use less than 30% of your available credit card limit.

- Credit Mix: A healthy balance between secured loans (like a home loan) and unsecured loans is viewed positively.

- Credit History Length: A long, positive track record of managing credit strengthens your profile.

- New Credit Inquiries: Frequent applications for new loans result in “hard inquiries,” which can temporarily lower your score and suggest “credit hunger”.

4. Quantitative Financial Ratios: How Much Can You Get?

Lenders don’t just decide if they should lend to you; they also decide how much. You should always compare personal loan platforms with transparent terms before choosing. This is determined using two primary methods: the FOIR and the Multiplier Method.

A. Fixed Obligation to Income Ratio (FOIR)

FOIR is a mathematical expression of your existing debt commitments relative to your monthly earnings.

- The Formula:

FOIR = [(Total Existing Monthly Debts + Proposed Loan EMI) / Net Monthly Income] x 100.

- Ideal Range: Most lenders prefer a FOIR between 40% and 55%.

- Example: If you earn ₹50,000 and your existing EMIs total ₹10,000, a lender will generally only allow your new personal loan EMI to be around ₹10,000 to ₹15,000 to keep the total below the 50% mark.

B. The Multiplier Method

This method provides a quick estimate of your loan eligibility based on your net monthly income.

- Standard Multipliers: Depending on your employer’s reputation and your credit score, lenders may offer 10x to 27x your monthly salary.

- Income Benchmark: Earning above ₹75,000 per month can often lead to interest rates that are 1%–2% lower than those offered to lower-income brackets.

5. The MoneyMonk Digital Advantage

Traditional borrowing can involve weeks of physical paperwork and branch visits. MoneyMonk has redefined this experience by leveraging technology. You can apply for a personal loan in minutes and get fast approval without delays, to provide a 100% digital journey.

Why Choose MoneyMonk?

- Speed: Approval is known instantly, and disbursement if approved is immediate, often taking just minutes.

- Loan Limits: We offer personal loans ranging from ₹30,000 to ₹3 Lakhs.

- Repayment Tenure: Flexible options ranging between 62 days to 180 days (2 to 6 EMIs).

- Transparency: All charges are communicated upfront via a Key Fact Statement; there are no hidden fees.

- Zero Document Upload: We utilize a compliant process where data is shared through your authentication and consent, eliminating the need to upload scanned copies of every document.

Eligibility Checklist for MoneyMonk:

- Citizenship: Must be an Indian Citizen.

- Age: Over 21 years old.

- Income: Stable monthly income above ₹18,000.

- Verification: Aadhaar must be linked with your PAN, and your mobile number must be linked with your Aadhaar for e-signing the agreement.

6. Detailed Documentation Requirements

Even in a digital-first world, lenders must verify your identity and financial capacity. Having these documents ready can significantly expedite the process.

For Salaried Borrowers:

- Identity Proof: PAN Card, Aadhaar Card, Passport, or Voter ID.

- Address Proof: Utility bills (not older than 2-3 months), Passport, or Rental Agreement.

- Income Proof: Salary slips for the last 3 months and Form 16.

- Financial Records: Bank statements for the last 6 months showing salary credits.

For Self-Employed Borrowers:

- Identity & Address Proof: Standard KYC documents.

- Business Continuity Proof: Certificate of Incorporation, GST registration, or Trade License.

- Income Proof: Income Tax Returns (ITR) for the past 2 to 3 years with computation.

- Financial Statements: Audited Profit & Loss (P&L) accounts and Balance Sheets.

- Banking: Business account statements for the last 6 to 12 months.

7. The Step-by-Step Approval Journey

Understanding the workflow helps you avoid common pitfalls and delays. Today, you can start your personal loan application instantly from your mobile with digital verification.

- Initial Application: You submit your basic details (age, income, employment) online.

- Instant Screening: Digital platforms like MoneyMonk conduct an immediate eligibility check.

- Credit Assessment: The lender fetches your CIBIL report to assess your repayment history.

- Digital Verification (e-KYC): Identity is verified through Aadhaar-based OTP or Video KYC.

- Final Offer: A sanction letter is issued detailing the approved amount, interest rate, and tenure.

- E-Signing & Disbursal: You digitally sign the loan agreement, and funds are disbursed directly into your bank account, often within minutes to a few hours.

8. Common Reasons for Loan Rejection (And How to Avoid Them)

Understanding why applications fail is just as important as meeting the criteria. Always choose transparent personal loan platforms with no hidden charges to avoid future issues.

- Low Credit Score: Scores below 650 lead to almost immediate rejection by prime lenders. Tip: Check your score regularly and dispute any errors on your report.

- Mismatched Documentation: Name or address discrepancies between your PAN, Aadhaar, and application form can derail your loan.

- High Debt-to-Income Ratio: If your FOIR exceeds 55%, lenders believe you won’t have enough disposable income to manage a new EMI.

- Unstable Employment: Job-hopping or being in a new job for less than 6 months raises suspicion.

- Incomplete KYC: Mismatched signatures or failed physical/digital address verification.

9. Specialized Eligibility Segments

The Indian financial sector has evolved to provide specialized criteria for diverse demographics.

A. Personal Loans for Women

Many lenders offer preferential pricing and simplified processing for women borrowers to encourage financial independence. This may include interest rate discounts (e.g., 0.05% lower). Even homemakers can establish eligibility by adding an earning co-applicant like a spouse or parent.

B. Personal Loans for Pensioners

Retirees can access funds where the “income” is a fixed pension.

- Age Limit: Repayment must typically be completed by the age of 76 to 78 years.

- Drawing Point: Most banks require the applicant to draw their monthly pension through a branch of the lending bank.

- Guarantor: A co-applicant, often a spouse or legal heir who will inherit the family pension, is usually mandatory.

C. Personal Loans for NRIs

Non-Resident Indians can manage domestic commitments in India through tailored loan products.

- Co-applicant Mandate: NRIs must have a resident Indian co-applicant (typically a spouse or parent).

- Repayment: Must be made through NRE or NRO accounts.

10. Pro-Tips to Boost Your Eligibility in 2026

If you want to secure the best possible terms and lowest interest rates, follow these expert strategies:

- Keep Your Score Above 750: This ensures you are viewed as a “low-risk” borrower, unlocking premium rates.

- Reduce Existing Debt: Pay off smaller loans or credit card balances before applying to lower your FOIR.

- Include a Co-applicant: If your individual income or credit score is on the borderline, adding a spouse or parent with a strong profile can bolster your application.

- Avoid Multiple Applications: Instead of applying with five different lenders, use comparison platforms to find the best match first, as multiple hard inquiries hurt your score.

- Apply During Salary Hikes: A recent bonus or salary increase improves your repayment capacity in the lender’s view.

- Maintain Job Stability: Stay with your current employer for at least a year before seeking a large personal loan.

If you want practical strategies to secure faster approvals and better loan terms, read our detailed guide on how to improve your personal loan approval chances fast

Conclusion: Building a Strong Financial Future

A personal loan is not just a static financial product; it is a conditional agreement based on your ongoing financial discipline. By understanding the granular eligibility criteria from the importance of a 750+ CIBIL score to the impact of your FOIR you position yourself to secure the most favorable credit terms available in the Indian market.

Ready to experience a modern way of borrowing? You can apply for a personal loan on the official website or download the app for instant approval and quick access. MoneyMonk offers a fast, transparent, and 100% digital journey tailored to your needs. Download the MoneyMonk app today and manage your money like a monk.

Disclaimer: All loan approvals are subject to credit assessment and terms and conditions of the lender.

Frequently Asked Questions (FAQs)

1. Can I get a personal loan with a low CIBIL score?

While possible, it is significantly more challenging. You may face higher interest rates (up to 36% or more) or be offered a smaller loan amount than requested. Focus on improving your score for 6-12 months before applying.

2. What is the minimum salary required for a personal loan in India?

Most lenders require a minimum monthly net salary of ₹15,000 to ₹25,000. At MoneyMonk, we require a stable monthly income of at least ₹18,000.

3. How long does it take for the loan to be disbursed?

Traditional banks may take 3 to 7 working days. Digital lenders like MoneyMonk can approve and disburse funds in minutes after the digital verification process is complete.

4. Is GST applicable on personal loans?

GST of 18% is applicable on the various fees and charges, such as processing fees and late payment penalties. However, GST is not charged on the interest component of your EMIs.

5. Can I get a personal loan without a salary slip?

Yes, some lenders accept bank statements showing regular salary credits as a substitute. Self-employed individuals must provide their latest ITRs instead.

Leave a Reply