Understanding the difference between a personal loan vs credit card loan can help you choose the best borrowing option in India. When a sudden financial requirement arises whether it is for a medical emergency, a wedding, a high-end gadget, or a planned home renovation most borrowers find themselves at a crossroads: should you opt for a personal loan or a credit card loan? If you are exploringinstant personal loan apps in India with fast approval, choosing the right option becomes easier. Both instruments offer immediate access to funds without the need for collateral, yet they operate on fundamentally different mathematical, regulatory, and structural foundations.

At MoneyMonk, we believe in managing your money with the discipline of a monk. Choosing the wrong borrowing method can lead to unexpected financial strain, trapping you in a cycle of debt that can severely impact your long-term savings and credit health. This comprehensive guide provides a strategic evaluation of these two credit options to help you make the most cost-effective decision for your financial future.

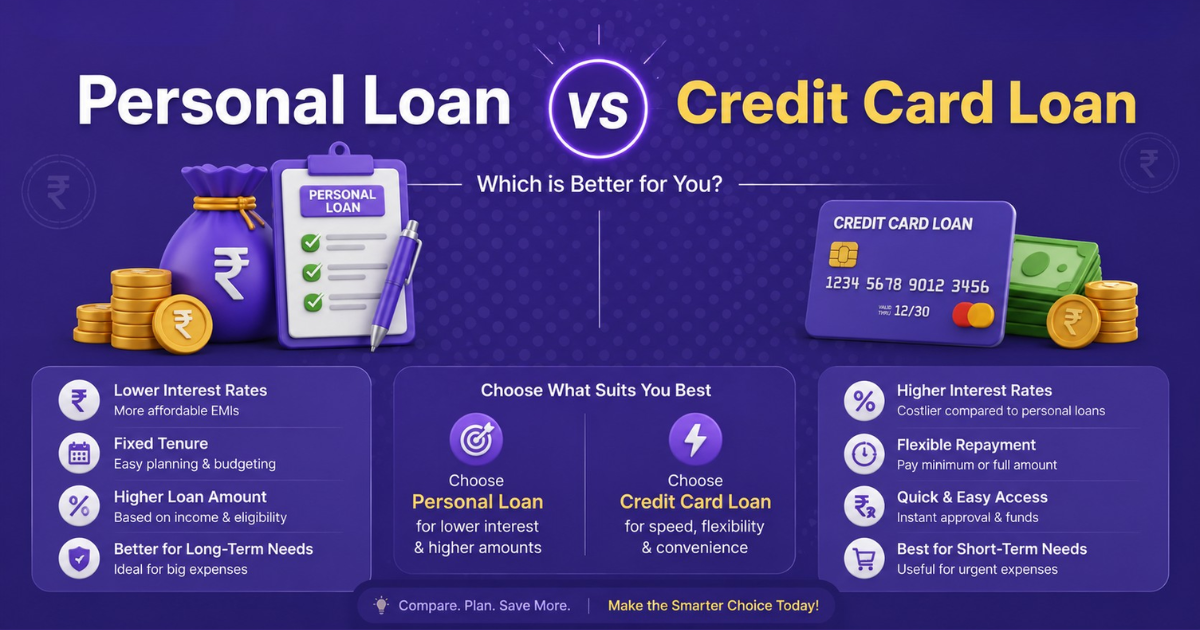

Understanding the Core Architectures: Personal Loans vs. Credit Card Loans

Before diving into the costs, it is essential to define what these products actually are and how they function in the modern Indian lending landscape.

What is a Personal Loan?

A personal loan is a type of unsecured installment credit where a lender provides a lump sum of money directly to your bank account. Today, you can apply for an instant personal loan online without paperwork through digital platforms. This amount is then repaid over a predetermined period, known as the loan tenure, through structured Equated Monthly Installments (EMIs). Personal loans are versatile and can be used for any financial need, ranging from debt consolidation to higher education.

What is a Credit Card Loan?

A credit card loan (often referred to as a loan against credit card or LACC) is a pre-approved debt facility offered by a bank based on your existing credit card limit and repayment history. Instead of being a standard purchase transaction, it is a separate loan sanctioned against the unutilized portion of your credit limit. These are marketed for their “instant” nature, as they often require zero additional documentation for existing cardholders.

Personal Loan vs Credit Card Loan Comparison

To determine which is “better,” we must analyze several critical parameters. It is always better to compare personal loan platforms with transparent terms before choosing that affect your pocket and your credit profile.

| Feature | Personal Loan | Credit Card Loan |

| Loan Nature | Lump-sum installment credit | Revolving/Term hybrid |

| Interest Rate Model | Usually lower (Reducing Balance) | Usually higher (Often Flat/Monthly) |

| Approval Time | Minutes (with MoneyMonk) to 7 days | Instant to 24 hours |

| Documentation | 100% digital KYC with MoneyMonk | Minimal to Nil for existing cards |

| Tenure | Flexible (up to 5–7 years) | Shorter (usually 3–24 months) |

| Credit Score Impact | Diversifies credit mix | Increases Credit Utilization Ratio |

| Processing Fee | Percentage-based (0.5%–3%) | Often flat or low for small amounts |

Deep Dive: Interest Rates and the Mathematics of Debt

The most significant differentiator is the cost of capital. Always choose transparent personal loan platforms with no hidden charges to reduce your total cost. While both are unsecured, they do not cost the same over time.

1. Interest Rate Benchmarks

In the 2025–2026 market, personal loan interest rates typically range from 10.50% to 24% per annum, depending on the borrower’s credit profile and income stability. At MoneyMonk, our dynamic interest rates start from 12% up to 36% per annum, specifically tailored to the risk profile and needs of salaried and self-employed professionals.

Conversely, credit card loan interest rates are frequently higher, often ranging between 15% and 24%, and can even exceed 36% per annum if you fail to clear your dues within the interest-free period.

Before applying, it is also important to understand lender income eligibility criteria, so read our detailed guide on minimum salary required for a personal loan

2. The Flat vs. Reducing Rate Trap

Borrowers often fall for the “flat rate” marketing trap.

- Personal Loans almost universally use the reducing balance method. Here, interest is calculated only on the outstanding principal. As you pay your EMIs, the principal reduces, and so does the interest component.

- Credit Card Loans frequently employ a flat interest rate. In this model, interest is calculated on the total sanctioned amount for the entire tenure.

Expert Insight: A 10% flat rate is statistically more expensive than a 14% reducing rate over the same period because the flat rate ignores the fact that you are paying back the principal every month.

Processing Speed and Convenience: When Seconds Count

For many, the choice isn’t just about the rate it’s about velocity. You can now start your personal loan application instantly from your mobile and get faster approvals.

- Credit Card Loans are unbeatable for absolute speed. Because the lender already has your KYC and spending data, funds can often be disbursed in a 10-second window.

- Traditional Personal Loans can take anywhere from 24 hours to 7 days as they involve fresh credit assessments and document verification.

- The MoneyMonk Advantage: We bridge this gap. Our 100% digital process allows you to receive approval and disbursal in under 15 minutes. By leveraging authentication and consent instead of scanned document uploads, we provide the speed of a credit card loan with the structured benefits of a personal loan.

Personal Loan vs Credit Card Loan: CIBIL Score Impact

Your credit score is your financial report card. Before applying, it is better to check your personal loan eligibility online instantly. and these two loan types affect it very differently.

Credit Utilization Ratio (CUR)

One of the biggest risks of a credit card loan is its impact on your Credit Utilization Ratio. If the loan is sanctioned “within the limit,” the amount is blocked from your available credit. This spikes your CUR, which is the proportion of revolving credit you are using. A CUR exceeding 30% is a major red flag for lenders and can pull your credit score down significantly.

Credit Mix and Discipline

A personal loan is an installment loan. Adding it to your profile improves your credit mix (the variety of debt you handle), which accounts for about 10% of your score. Since it follows a fixed EMI schedule, timely repayments demonstrate long-term financial discipline, helping to boost your score over time.

Hidden Costs: Fees, Penalties, and GST

The advertised interest rate is only one part of the story. You should always choose trusted digital personal loan platforms with full transparency. You must look at the Effective Annual Cost.

- Processing Fees: Personal loans usually charge 0.5% to 3% of the loan amount. Credit card loans often have smaller, flat fees (e.g., ₹500), making them cheaper for small amounts under ₹1 lakh.

- Foreclosure Charges: If you want to pay off your debt early, personal loans often have a lock-in period and charges of 2% to 5% on the outstanding principal. While new regulations are moving toward removing these for floating-rate loans, most unsecured personal loans remain fixed-rate. Credit card loans also carry foreclosure fees (typically 3%), but often lack long lock-in periods.

- GST Impact: In India, an 18% GST is applicable on all fees for both products. However, on some credit card EMI products, GST may even be applied to the monthly interest portion, an extra cost that doesn’t exist for standard personal loans.

Personal Loan vs Credit Card Loan: Which Should You Choose?

As an expert, I recommend selecting your credit product based on the urgency, amount, and duration of the need. You can manage your personal loan journey smartly using digital tools for better decisions.

Choose a Personal Loan (and MoneyMonk) if:

- You need a larger amount: If you require more than ₹1 lakh for a major expense like a wedding or home renovation.

- You want lower interest: You prefer a predictable, reducing-balance interest rate to save on total outgo.

- You need a longer tenure: You want to spread repayments over 12 to 60 months to keep your monthly EMIs manageable.

- You are consolidating debt: You want to use a low-interest loan to pay off multiple high-interest credit card debts.

Choose a Credit Card Loan if:

- It’s a minor, urgent emergency: You need ₹25,000 to ₹50,000 instantly for a repair or immediate bill.

- You can repay quickly: You plan to clear the debt within 3 to 12 months.

- You find a “No-Cost EMI” deal: You are making an e-commerce purchase where a merchant discount offsets the interest, effectively giving you 0% interest.

- Convenience is the priority: You already have a card and want zero paperwork.

Why Borrow with MoneyMonk?

Traditional banks often involve a “pile of paperwork” and lengthy approval processes. At MoneyMonk, we have reimagined the personal loan journey for the digital age.

- Proprietary NBFC: We are operated by Monk Capital Pvt Ltd, an RBI-registered NBFC, ensuring 100% compliance and security.

- Speed: Disbursement is done in minutes following approval.

- Transparency: All charges are disclosed upfront via a Key Fact Statement. No hidden fees.

- Flexibility: We offer loans ranging from ₹25,000 to ₹2 Lakhs with repayment tenures between 62 days to 180 days.

- Data Privacy: Your data is yours. We use masked documents and consent-based data sharing.

Expert Conclusion: Which is the Smartest Choice?

In the strategic battle of Personal Loan vs. Credit Card Loan, the personal loan is almost always the superior choice for planned, high-value expenditures. It offers lower interest rates, longer tenures, and a positive impact on your credit mix without damaging your credit utilization.

However, the credit card loan remains a powerful liquidity buffer for small, time-sensitive emergencies.

The key to financial freedom is not just borrowing, but borrowing responsibly. Always compare the total interest outgo and the processing fees before signing any agreement.

Ready to manage your money like a monk?

You can apply for a personal loan on the official website or download the app for instant approval and quick access. and experience a 100% digital personal loan journey that puts you in control.

Frequently Asked Questions (FAQs)

No. A credit card loan is generally classified as an unsecured personal loan sanctioned against a revolving credit line. Unlike standard term loans, it doesn’t always require a lump-sum commitment from a business perspective.

Yes, most lenders allow foreclosure. However, check for prepayment penalties, which can range from 2% to 5% of the outstanding principal. Some digital lenders like MoneyMonk have specific policies for loan closure that emphasize transparency.

Effectively, yes, for your pocket—but technically, no. The interest is usually offset by a discount given by the merchant. Note that you still have to pay 18% GST on the interest amount to the bank.

MoneyMonk is 100% digital and compliant. We do not require scanned document uploads; all data is shared through your authentication and consent. Documents are masked, and privacy is our top priority.

Missing an EMI is serious. It results in late payment charges (at MoneyMonk, this is a 36% annualized penal charge) and a significant negative impact on your credit score. It also makes you ineligible for higher-value loans in the future.

Leave a Reply