Understanding personal loan interest rates helps borrowers choose the right loan and reduce total borrowing costs in India. Navigating the world of personal finance can often feel like trying to solve a complex puzzle with missing pieces. When you apply for a personal loan, the single most important number you look for is the interest rate. If you are exploring instant personal loan apps in India with fast approval, understanding interest calculation becomes even more important. But have you ever wondered why one person gets an offer at 10% while another is quoted 18%? Or why your monthly payment doesn’t seem to match the advertised rate?

Understanding the “black box” of interest rate calculation is not just for bankers; it is a vital skill for every borrower. In this comprehensive guide, we will pull back the curtain on how financial institutions determine their rates, the structural mechanics behind the Indian banking sector, and how you can position yourself to get the best deal. At MoneyMonk, we believe that transparency is the foundation of financial wellness, and that starts with education.

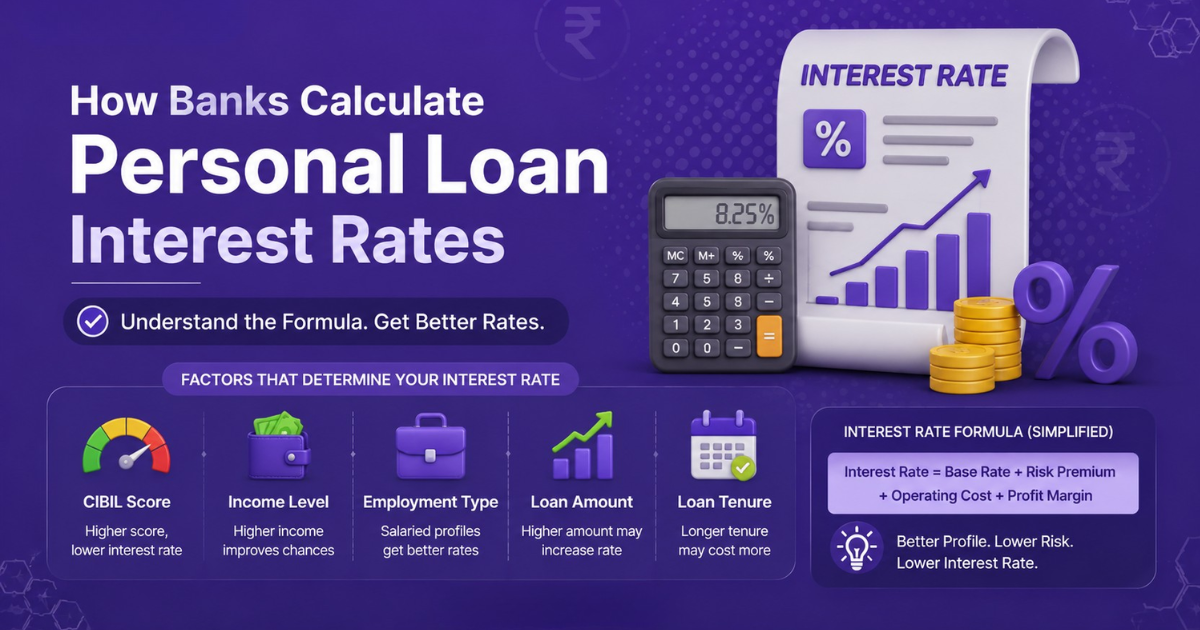

1. How Personal Loan Interest Rates Work

A personal loan is a form of unsecured credit, meaning it does not require you to pledge any collateral like a house or gold. Because the lender takes on a higher risk there is no asset to seize if the borrower defaults the interest rates are typically higher than those of secured loans.

The interest rate is the percentage charged by a lending institution on the principal amount you borrow. This percentage is the primary driver of:

- Your Equated Monthly Installment (EMI): The fixed amount you pay every month.

- The Total Cost of Borrowing: The sum of all interest paid over the life of the loan.

- Your Financial Flexibility: A high rate can strain your monthly budget, while a lower rate allows for better financial planning.

Even a small difference of 1% or 2% in your interest rate can result in thousands of rupees in savings or extra costs. That’s why it is better to compare personal loan platforms with transparent interest rates before applying over a 3- to 5-year tenure.

2. The Evolution of Benchmarking: How Rates Have Changed

To understand how rates are calculated today, we must look at how the Reserve Bank of India (RBI) has regulated lending benchmarks. Choosing RBI-compliant digital personal loan platforms like MoneyMonk ensures better transparency. over the last decade. The goal has always been transparency and the rapid transmission of policy changes to the end borrower.

The Three Pillars of Benchmarking

| Feature | Base Rate (Pre-2016) | MCLR (2016–2019) | EBLR (2019–Present) |

| Primary Driver | Average cost of funds | Marginal cost of funds | External benchmarks (e.g., Repo Rate) |

| Transparency | Low (Internal policy) | Moderate (Standardized components) | High (Publicly available) |

| Transmission Speed | Very slow | Moderate | High/Immediate |

| Reset Frequency | Annual or longer | 6 to 12 months | Quarterly (usually 3 months) |

The Base Rate Era

Before 2016, banks used the Base Rate system, which was based on the average cost of funds. This system was rigid and often failed to reflect real-time changes in the economy, leaving borrowers with high rates even when the RBI was cutting interest.

The MCLR Revolution

Introduced on April 1, 2016, the Marginal Cost of Funds Based Lending Rate (MCLR) shifted the focus to the incremental cost of arranging every additional rupee of deposit. While more transparent, it still had a delay in transmitting rate cuts because resets only happened every 6 to 12 months.

The Contemporary EBLR Standard

To ensure immediate benefits for borrowers, the RBI mandated the External Benchmark Lending Rate (EBLR) for new retail loans starting October 1, 2019. Under this regime, rates are pegged directly to external indicators like the RBI’s Repo Rate.

3. Personal Loan Interest Rates and MCLR

While EBLR is the current standard for many new loans, MCLR remains a critical internal benchmark for many existing personal loans and specific credit categories. The calculation of MCLR is a precise function of four variables. Instead of understanding complex calculations manually, you can apply for a personal loan online with simplified digital processes:

The MCLR Formula

MCLR=MCOF+Negative Carry on CRR+Operating Costs+Tenor Premium

- Marginal Cost of Funds (MCOF): This is the heart of the formula, accounting for roughly 92% of the total. it includes the interest rates offered on various deposits and the bank’s return on net worth.

- Negative Carry on Cash Reserve Ratio (CRR): Banks must keep a percentage of their deposits with the RBI at 0% interest. The “negative carry” is the cost the bank incurs to acquire these non-earning funds, which is then passed on as a small markup.

- Operating Costs: These are the administrative expenses of running a bank, including salaries, rent, and digital infrastructure.

“ - Tenor Premium: Longer-term loans carry a higher risk of volatility, so banks apply a premium based on the duration of the loan.

Banks publish a suite of MCLR rates for different tenors (Overnight, 1-month, 3-month, 6-month, 1-year). Most personal loans are linked to the 1-year MCLR.

5. Personal Loan Interest Rates Under EBLR

The External Benchmark Lending Rate (EBLR) is far more dynamic. Today, digital platforms allow you to start your personal loan application instantly from your mobile with updated rates. Instead of relying on a bank’s internal costs, it looks at the broader market.

The EBLR Formula

FinalRate=ExternalBenchmark(RepoRate)+Credit Risk Premium (CRP)+B

The Repo Rate is the rate at which the RBI lends money to commercial banks. When the RBI changes this rate, your EBLR-linked loan interest rate typically adjusts within 3 months, providing immediate impact.

Under this regime, banks are prohibited from modifying the “spread” (the CRP and BSP) for the duration of the loan unless your credit profile changes significantly. This provides a layer of protection and predictability for the borrower.

5. The Secret Sauce: Understanding the “Spread”

The benchmark (MCLR or EBLR) provides the foundation, but the spread is what customizes the rate to you. This is why two people can apply at the same time and get different rates. You can check your personal loan eligibility online instantly to understand your chances before applying.

Credit Risk Premium (CRP)

This is a quantitative reflection of your probability of default. Since personal loans are unsecured, lenders rely heavily on your creditworthiness.

- Credit Score: A score above 750 often puts you in a “low-risk bucket,” resulting in a minimal CRP. A score below 600 might double your CRP or lead to rejection.

- Income Stability: Salaried employees in stable sectors (like government or MNCs) are perceived as lower risk than freelancers or those in small enterprises.

- Debt-to-Income (DTI) Ratio: Lenders look at how much of your monthly income is already committed to existing debt. A DTI ratio under 40% is usually required for the best rates.

Business Strategy Premium (BSP)

This is a discretionary markup that allows the lender to remain competitive while maintaining profit margins.

- Relationship Discounts: Loyal customers with existing accounts or a good repayment history may receive a discount on the BSP.

- Target Demographics: Lenders often run special schemes for women, senior citizens, or specific professions like doctors, offering slightly lower BSPs.

- Loan Size: Larger loans often have lower interest rates because the fixed processing costs are spread over a larger interest-earning principal.

6. Personal Loan Interest Rates: Flat vs Reducing

One of the most common pitfalls for borrowers is failing to distinguish between flat and reducing interest rates. Always choose transparent personal loan platforms with no hidden charges to avoid extra costs. This one detail can double the actual cost of your loan.

Flat Interest Rate

In this system, interest is calculated on the original principal amount for the entire tenure. Even as you pay back the loan, you are still paying interest on the full amount you borrowed on day one.

- Pros: Easy to calculate, predictable payments.

- Cons: Significantly more expensive in the long run.

Reducing (Diminishing) Balance Interest Rate

Interest is calculated only on the outstanding principal balance. As you pay your installments, the principal decreases, and so does the interest component for the next month.

- Pros: The standard for most transparent lenders; mathematically fair and much cheaper.

- Cons: More complex manual calculation (though online calculators make this easy).

The Cost Comparison (₹5,00,000 Loan at 12% for 3 Years)

| Factor | Flat Interest Rate System | Reducing Balance System |

| Calculation Base | Initial ₹5,00,000 | Decreasing Balance |

| Monthly EMI | ₹19,444 | ₹16,607 |

| Total Interest Paid | ~₹1,80,000 | ₹97,852 |

| Effective Annual Rate | ~21.5% | 12.0% |

The difference is clear: A 12% flat rate is actually as expensive as a 21.5% reducing rate. Always ask your lender to confirm if the rate is monthly reducing.

7. Fixed vs. Floating Rates: Which Should You Choose?

When applying, you will likely have to choose between a fixed and a floating interest rate.

- Fixed Interest Rates: The rate remains locked for the entire tenure. Your EMI will never change, making it ideal for those who want total budget certainty. However, fixed rates are often slightly higher than initial floating rates.

- Floating Interest Rates: The rate fluctuates based on the benchmark (Repo or MCLR). If market rates drop, your EMI or tenure could decrease. If market rates rise, your loan becomes more expensive.

MoneyMonk Tip: For short-term personal loans (under 2 years), a fixed rate often provides the best peace of mind. For longer tenures, a floating rate might allow you to benefit from future economic shifts.

8. The True Cost of a Loan: APR and the KFS

Looking only at the interest rate is like looking at the price tag of a car without checking the taxes, registration, and insurance. To know what you are really paying, you need two things: the APR and the KFS. Choosing trusted digital personal loan platforms with full transparency helps you avoid hidden charges.

Annual Percentage Rate (APR)

The APR represents the total yearly cost of borrowing, including the interest rate plus all mandatory fees (processing fees, documentation charges, insurance, etc.).

- Formula: APR= Interest+Fees/Loan Amount x Tenure x 365 x 100

- Why it matters: It allows you to compare two lenders fairly. For example, Lender A might have a 10% rate but a 4% fee, while Lender B has an 11% rate but zero fees. The APR will tell you which one is actually cheaper.

Key Fact Statement (KFS)

Effective October 2024, the RBI has made the Key Fact Statement mandatory for all personal loans. This is a simple, one-page document that summarizes the most critical loan terms in plain language.

A valid KFS must include:

- Loan Amount & Tenure.

- APR (Total Cost of Credit).

- Detailed Fee Structure (Processing, Documentation, etc.).

- Repayment Schedule (Monthly breakdown).

- Contingent Charges (Late payment or bounce penalties).

- Cooling-off Period: A window (at least 1 day) during which you can cancel the loan without penalty.

Always insist on seeing the KFS before you sign anything.

9. 5 Factors That Influence Your Personal Loan Interest Rate

While banks have their structural formulas, your personal profile determines the final number on your offer. Here is how to optimize it. You can manage your personal loan journey smartly using digital tools to improve approval chances.:

- Credit Score (The Gold Standard): A score of 750 or higher is generally the threshold for premium rates. Maintain this by paying credit card bills on time and avoiding too many loan inquiries in a short period.

- Income and Employment: Lenders prefer “guaranteed” income. If you have been with the same employer for over 2 years, you are seen as more stable.

- Debt-to-Income Ratio: If 50% of your salary already goes to EMIs, you are high risk. Try to clear smaller debts before applying for a major personal loan.

- Relationship with the Lender: Being an existing customer (holding a salary account or having a previous clean loan) can get you a “loyalty discount” of 0.25% to 0.75%.

- Employer Reputation: Working for a listed company, a PSU, or a large MNC often gets you lower rates because these firms are seen as more financially stable.

If you want to maximize your approval chances and secure better loan terms, read our complete guide on how to boost personal loan approval chances

10. Practical Strategies to Lower Your Interest Burden

If you find your quoted rate is too high, don’t lose hope. Here is how to negotiate and plan:

- Improve Your Credit Score First: If your score is currently 680, wait 3–6 months while you clear card balances. Moving your score to 750 can save you significant interest over a 5-year loan.

- Opt for a Shorter Tenure: While a 5-year loan has a lower EMI, the total interest you pay is exponentially higher than a 2- or 3-year loan.

- Negotiate the Fees: Processing fees and insurance add-ons are often negotiable. Ask for a waiver or a discount.

- Prepay When Possible: If you get a bonus or extra savings, pay off a part of your principal. This reduces the base for interest calculation and can cut your tenure significantly.

- Use a Co-Applicant: If your income is low or your credit score is average, adding a co-applicant (like a spouse) with a strong profile can secure a lower rate.

11. Manage Your Money Like a Monk: The MoneyMonk Advantage

At MoneyMonk, we believe that getting a loan should be a tool for growth, not a source of stress. You can apply for a personal loan in minutes and get fast approval without delays. We offer a 100% digital, transparent journey tailored for the modern borrower.

Why Choose MoneyMonk?

- Speed and Convenience: Our process takes as little as 5 minutes, from application to approval.

- Dynamic Interest Rates: Rates start from 12% p.a., depending on your risk profile, with zero hidden charges.

- Education Fee Financing: We specialize in helping you invest in your future with specialized fee payment options.

- Regulatory Compliance: We are an RBI-registered NBFC, ensuring that every loan is governed by fair practice codes and clear disclosure.

- Privacy Secured: We use digital authentication to ensure your documents are masked and your data is always protected.

With loan amounts ranging from ₹25,000 to ₹2 Lakhs and flexible tenures of 62 to 180 days, MoneyMonk is designed for those who need quick, reliable, and honest financial support.

12. Conclusion: Knowledge is Your Best Asset

Calculating personal loan interest rates is a science that combines global economic policy with your individual financial habits. By understanding the difference between MCLR and EBLR, knowing the importance of your DTI ratio, and always looking for the Reducing Balance rate, you are no longer at the mercy of complex jargon.

Before you take your next loan, use an EMI calculator, review your Key Fact Statement, and ask the right questions. A well-planned loan is the first step toward long-term financial freedom.

Ready to manage your money like a monk? Download the MoneyMonk app today and experience the future of digital lending.

Frequently Asked Questions (FAQs)

The interest rate only covers the cost of the principal amount. The APR includes the interest rate plus mandatory fees like processing charges and insurance. It represents the total “all-in” cost.

Yes, most lenders allow you to switch from an internal benchmark (MCLR) to an external one (Repo-linked) for a nominal conversion fee. This is often beneficial in a falling interest rate cycle.

Often, yes. Lenders offer lower rates for bigger loans (e.g., above ₹2 lakh) because the administrative costs are fixed, making the loan more profitable for them at a slightly lower margin.

It is a regulatory mandate where you are given at least one day after signing the agreement to cancel the loan without paying any prepayment penalty. You only pay the principal and the interest for the days you held the money.

A single EMI default can drop your credit score and mark you as “high risk”. In the future, lenders will likely charge you a higher Credit Risk Premium, making all your future loans more expensive.

Leave a Reply